Corporation tax rates are changing for corporation tax years, starting on 1 April 2023. From this date, there will no longer be a single corporation tax rate for non-ring-fenced company profits.

We don’t often see a universal approach to tax in the business world. Corporation Tax has to date, been something that falls into this category from 2014/2015 when marginal relief was last applied. The tax rate for company profits prior to 1 April 2023 was 19% no matter the amount of profits. From the 1st April 2023, this will no longer apply, and the rate at which companies pay corporation tax will depend on the level of their profits.

What does this mean for your business;

- The small profits tax rate will be 19% for profits of £50,000 or less.

- The tax rate for profits more than £250,000 is increased to 25%.

- Companies with profits between £50,000 and £250,000 pay the main rate of 25%, reduced by marginal relief. This is to provide a gradual increase in the effective rate of tax between £50,000 and £250,000.

The practical impact of this is that corporation tax will be payable at 19% on profits up to £50,000 and will payable at an effective rate of tax rate of 26.5% on profits between £50,001 -£250,000.

What is Marginal Relief?

You can reduce your Corporation Tax bill through Marginal Relief from 1 April 2023 if your company’s profits are lower than £250,000. This provides a gradual increase in Corporation Tax rate between the small profits rate and the main rate, allowing you to reduce your rate from the 25% main rate.

Who can claim Marginal Relief?

Your company or organisation may be able to claim Marginal Relief if its taxable profits from 1 April 2023 are between:

- £50,000 (the lower limit)

- £250,000 (the upper limit)

If your accounting period is shorter than 12 months these limits are proportionately reduced. These limits are also proportionately reduced by the number of associated companies your company has. More information on associated companies can be found on the GOV.UK website. Marginal Relief for Corporation Tax – GOV.UK (www.gov.uk)

Associated Companies

Very broadly speaking, an associated Company is another Company which you, or as a group of the same shareholders, have control of. If you have an associated Company, then the tax bands above are divided by the total number of Companies under your control. So, if you had 4 Companies the small profits tax limit of £50,000 will be reduced to £12,500 (£50,000 divide by 4) for each Company which means you start to pay a higher rate of tax earlier.

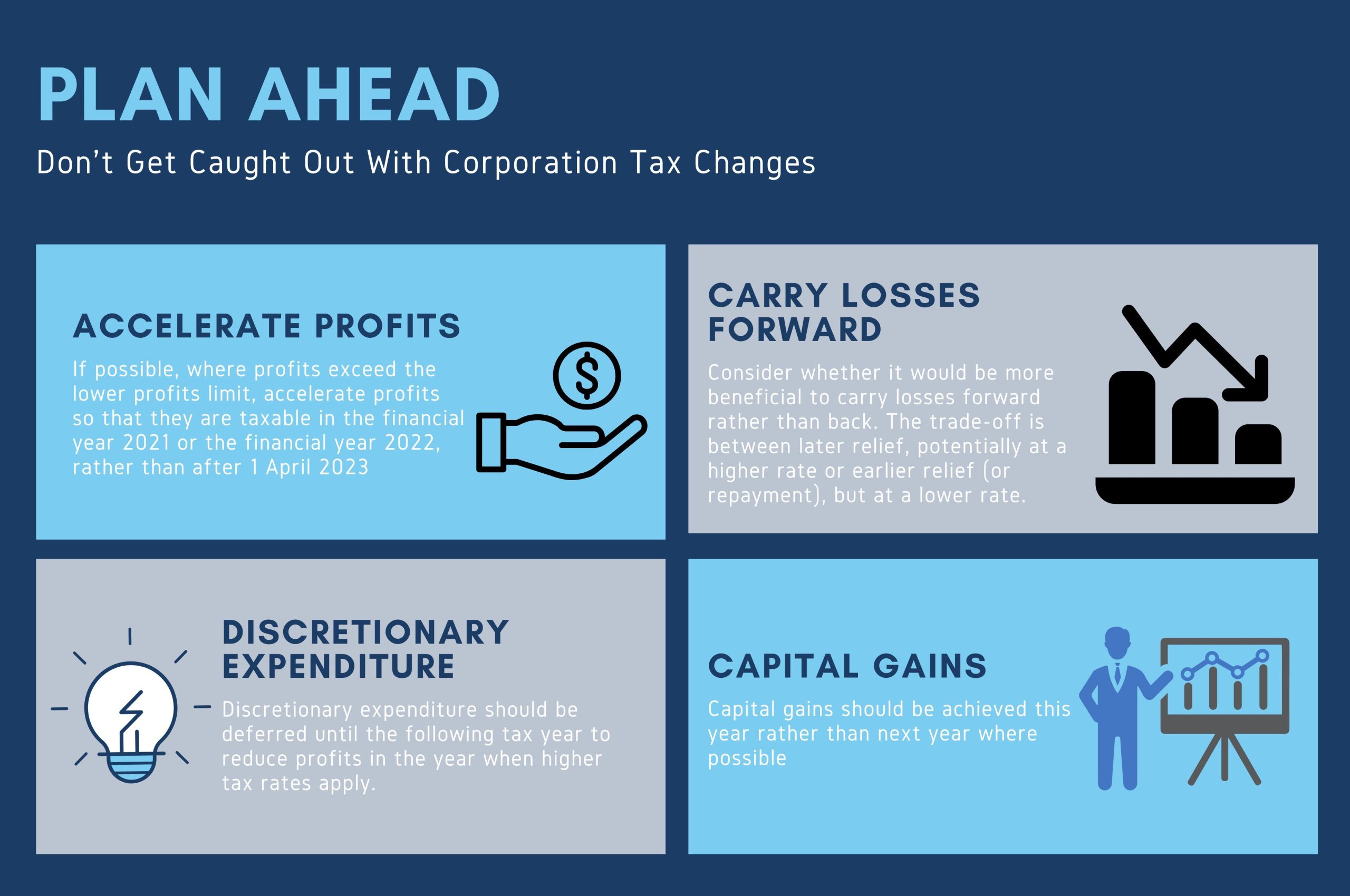

How to manage the increase in tax

As with any increase in outgoings, it is important to plan how your business will manage this, and there is thankfully still time to plan ahead.

Super-deductions finish March 2023

The super-deduction tax break that was introduced on 1 April 2021 is coming to an end on 31st March 2023.

This tax break allows businesses to;

- deduct 130% of the cost of any qualifying investment on most new plant and equipment investments that would ordinarily qualify for 18% main rate writing down allowances.

- a 50% first-year allowance for qualifying special rate assets

The super-deduction will allow companies to cut their tax bill by up to 25p for every £1 they invest, ensuring the UK capital allowances regime is amongst the world’s most competitive.

Capital investment must be in new and unused assets that qualify as main pool expenditure, subject to some specific exclusions. This will include expenditure such as solar panels, tractors, lorries and vans, fire alarm systems, security systems, carpets, computer equipment and servers, office desks and furniture, refrigeration units and electric vehicle charging points.

The rate of the super-deduction will require apportioning if an accounting period straddles 1 April 2023. The rate should be allocated based on days falling prior to 1 April 2023 over the total days in the accounting period.

Apart from the enhanced expenditure, another positive aspect of the super-deduction is that there is no cap.

Next Steps

The UK’s corporation tax rate is currently 19% and is continuously increasing. It is essential to be tax compliant, pay less corporation tax and receive the most tax relief possible. Seeking professional advice is the best option if you need help with your corporation tax. Contact us today and book in for one of our dedicated ‘Corporation Tax Consultation’ meetings – info@exchangeaccountants.com

Sources – Corporation tax changes from 1 April 2023: Plan ahead – Tax Insider, Marginal Relief for Corporation Tax – GOV.UK (www.gov.uk) Corporation tax changes: 2023 | Croner-i (croneri.co.uk), Ten things you need to know for super-deduction | ACCA Global, Super-deduction – GOV.UK (www.gov.uk)